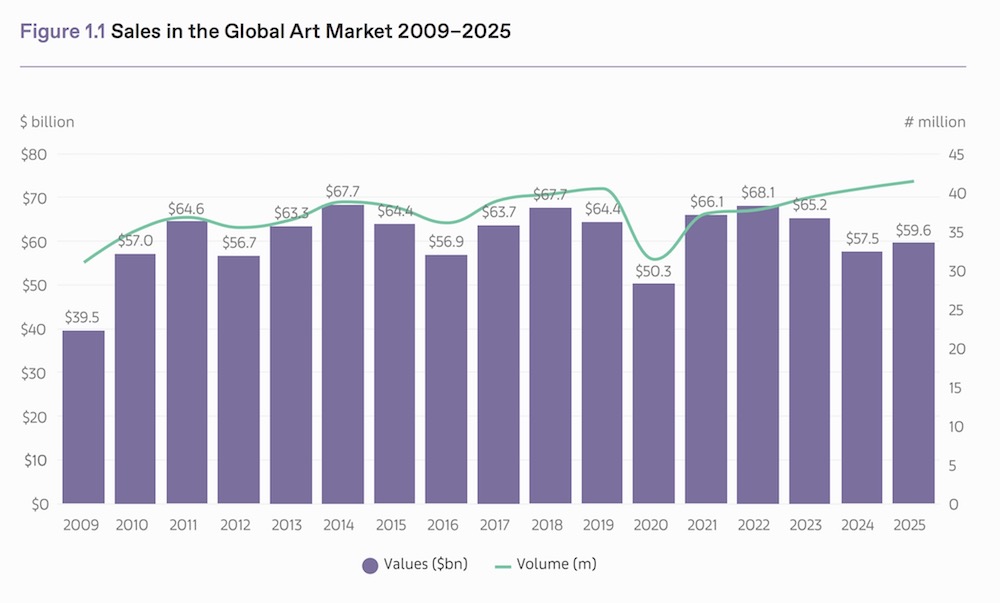

Markets rarely move independently of the societies that sustain them. The global art market is no exception. It reflects wealth, confidence, cultural priorities, and geopolitical realities, often serving as a barometer of broader economic and social change. According to The Art Basel and UBS Art Market Report 2026, global art sales rose by 4% in 2025 to an estimated $59.6 billion, marking the first year of growth since 2022. While modest, the increase represents a significant reversal after two consecutive years of contraction and suggests that the market has entered a period of cautious recovery.

The figures nevertheless require perspective. Despite the improvement, the market remains below its post-pandemic peak of $68.1 billion achieved in 2022 and is still smaller than it was a decade ago. Since 2015, the market has declined by 7% in value. What emerged in 2025 was not a return to the exuberance of the post-pandemic boom, but rather evidence of a sector adapting to a more demanding economic environment.

The year began under difficult circumstances. Geopolitical tensions, armed conflicts, trade disputes and concerns surrounding economic fragmentation weighed heavily on sentiment. Uncertainty intensified following the return of tariff-related trade disputes associated with the United States. Dealers, auction houses and collectors faced a marketplace shaped by rising costs, unpredictable policy decisions and heightened caution among sellers.

Yet conditions improved significantly during the second half of the year. Stronger supply at the top end of the market, renewed activity at major international art fairs and several high-profile auction consignments contributed to a noticeable shift in confidence. High-value transactions led the recovery, particularly works selling for more than $10 million.

Global Art Market 2026: Recovery, Realignment and the Search for Stability Chart Courtesy Art Basel

Public auctions recorded the strongest gains, rising by 9% year-on-year. Dealer sales also improved, rising 2% to $34.8 billion. In contrast, private sales at auction houses declined by 5%, reversing a pattern that had characterised the previous year. The change suggests that sellers were once again willing to expose works to public competition, reflecting greater confidence in market conditions.

Transaction volumes told a different story. The total number of transactions increased by just 2% to 41.5 million. This relative stability contrasts with earlier downturns, particularly during the global financial crisis, when sharp declines in activity accompanied falling values. The market’s resilience at lower price levels helped maintain volume even as values fluctuated.

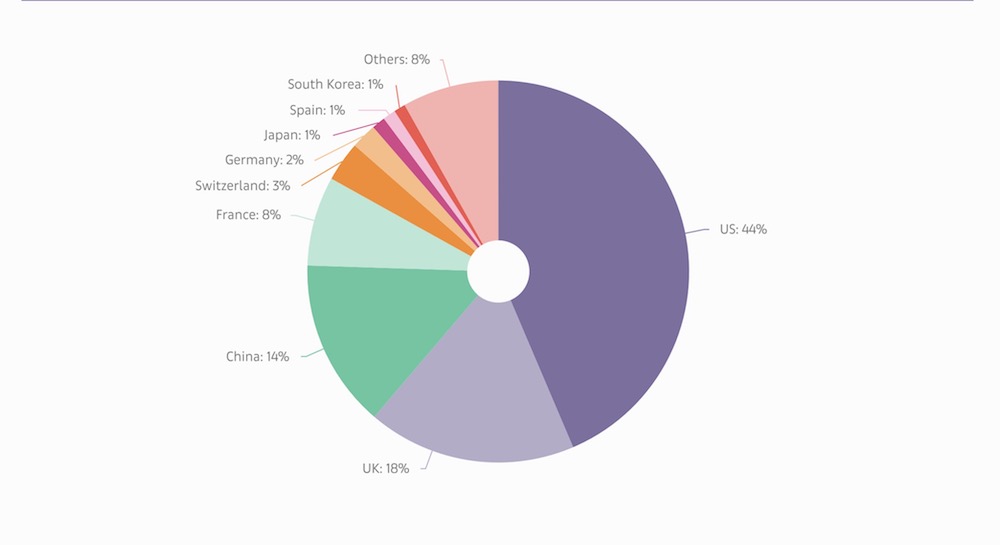

The United States remained the dominant global art market, accounting for 44% of worldwide sales. Total sales reached $26 billion, representing a 5% increase after two years of decline. Much of this growth was driven by the high end of the market, where auction sales of works exceeding $10 million increased by nearly 40%. Despite ongoing concerns over tariffs and trade policy uncertainty, the United States retained its position as the primary centre for major transactions.

The United Kingdom maintained its second-place position globally, accounting for 18% of sales. The market grew by 2% to $10.5 billion, although figures remain below pre-pandemic levels. Public auction activity strengthened, but dealer sales remained relatively subdued.

China remained the third-largest art market, accounting for 14% of global sales, valued at $8.5 billion. Growth was minimal at just over 1%. The market reflected contrasting regional dynamics. Mainland China experienced stronger auction activity, while Hong Kong faced continued challenges amid weaker international demand. Economic pressures linked to the country’s prolonged property downturn continued to affect collector confidence.

Global Art Market 2026: Recovery, Realignment and the Search for Stability Chart Courtesy Art Basel

France enjoyed one of the strongest performances among major markets. Sales rose 9% to $4.5 billion, pushing the market slightly above its 2019 level. Elsewhere in Europe, Switzerland and Austria recorded gains of 13%, while Spain increased by 6%. Germany and Italy, however, experienced declines of 10% and 2% respectively.

One of the report’s most striking observations concerns the changing structure of the gallery sector. Despite several prominent gallery closures attracting headlines throughout the year, the broader picture proved more resilient. New gallery openings exceeded closures overall, suggesting continued confidence among entrepreneurs and dealers. Arts Economics surveyed more than 1,650 dealers across seventy markets and found that many businesses were adjusting operations in response to rising costs rather than retreating altogether.

Most dealers continue to demonstrate remarkable longevity compared with businesses in other sectors. The average gallery has operated for twenty-six years, significantly longer than the average lifespan of companies in both the United States and the United Kingdom. Nevertheless, many galleries have consolidated their operations, reducing the number of physical locations they maintain.

Art fairs strengthened their position within the commercial ecosystem. Their share of dealer sales rose from 31% in 2024 to 35% in 2025, confirming the continued importance of face-to-face engagement. While digital platforms remain important, the market’s enthusiasm for in-person encounters appears to have returned decisively.

Online sales declined to $9.2 billion, representing 15% of the market. This was the lowest figure since 2019 and well below the pandemic peak of 25% achieved in 2020. The shift reflects a broader rebalancing between the convenience of digital transactions and the experiential nature of art buying. Collectors increasingly returned to fairs, exhibitions and live auctions, especially for higher-value acquisitions.

The auction sector experienced a notable revival. Strong consignments and several important single-owner collections drove significant growth. The most spectacular result was Gustav Klimt’s Portrait of Elisabeth Lederer, which sold for $236.4 million at Sotheby’s New York. The work set a new auction record for the artist and became the second-most-expensive artwork ever sold at auction.

Other standout results included Vincent van Gogh’s Piles de Romans Parisiens et Roses dans un Verre at $62.7 million, Mark Rothko’s No. 31 (Yellow Stripe) at $62.2 million and Frida Kahlo’s El Sueño (La Cama), which achieved $54.7 million. The value of the top fifty auction lots increased by 30% year-on-year, while the top ten rose by 48%.

The report also highlights generational change among collectors. Christie’s reported that 46% of new bidders and buyers were millennials or members of Generation Z. Luxury categories continued to attract new participants, accounting for 38% of first-time buyers.

At the same time, significant inequalities remain. Progress in gallery representation continued, with women accounting for 45% of artists represented by dealers, a four-point increase year-on-year. Primary market galleries reached gender parity on average. However, the auction market remains heavily skewed. Only 11% of artists appearing in the top 200 auction rankings were women, accounting for just 8% of sales value.

Even among female artists, commercial success remains concentrated in the hands of a handful of names. Joan Mitchell, Yayoi Kusama, Agnes Martin, Marlene Dumas and Cecily Brown together accounted for more than half of all auction value generated by female artists in the Postwar and Contemporary sectors.

Looking ahead, the report presents a cautiously optimistic outlook. UBS identifies several long-term forces likely to shape future collecting patterns, including technological innovation, artificial intelligence and the so-called Great Wealth Transfer, which is expected to see more than $83 trillion pass between generations in the coming decades. These developments are already influencing collecting behaviour, philanthropy and cultural engagement.

The central conclusion of The Art Basel and UBS Art Market Report 2026 is that the market’s recovery represents more than a simple return to growth. It signals a period of adjustment in which businesses, collectors and institutions are recalibrating their expectations. The market remains vulnerable to geopolitical instability, rising costs and economic uncertainty. Yet it has demonstrated resilience, adaptability and a renewed capacity for growth. In that sense, 2025 may ultimately be remembered not as the year the art market recovered, but as the year it began to redefine itself.

Download The Full Report Here